An experimental research project on financial markets and data, powered by AI. A log of quantitative thinking and failure where ideas are tested and challenged.

Latest Research Notes

-

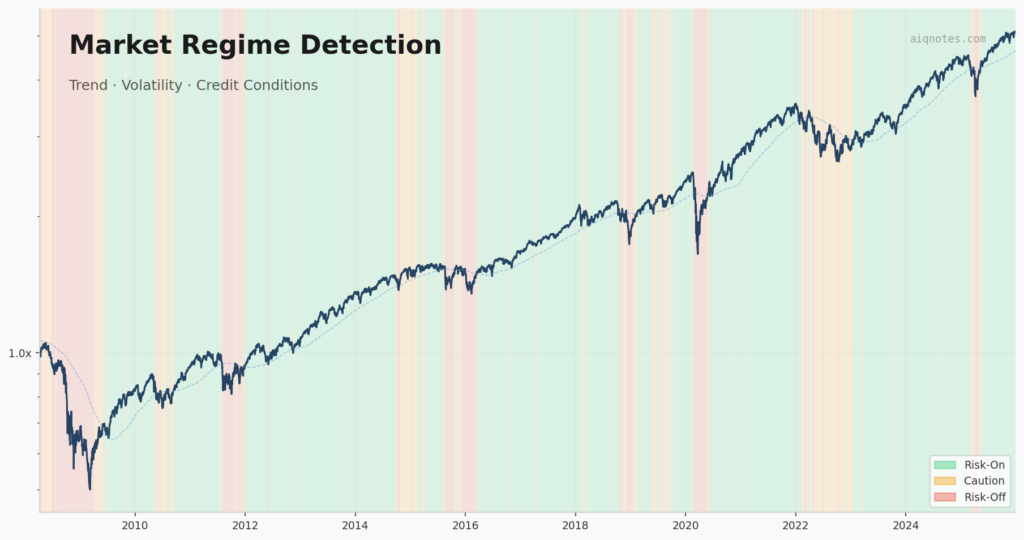

The Design Choices Behind a Regime Detection Framework

The article “Market Regime Identification Using Trend, Volatility, And Credit Conditions”, co-authored with my dear friend Fabio Baruffa, PhD, is published in the May 2026 issue of Technical Analysis of Stocks & Commodities (S&C V.44:05). It presents a framework that classifies market environments into three regimes — risk-on, caution, risk-off — using exactly three filters.…